On June 16, SpaceX agreed to buy Cursor, the AI coding company, for $60 billion in stock. CNBC reported the all-stock deal will close in the third quarter of 2026, carrying a $10 billion break fee that falls to $4 billion if it collapses on antitrust grounds. Most of the coverage filed it under the AI coding race against OpenAI and Anthropic.

That framing is too small. The deal landed four days after SpaceX raised $75 billion in the largest IPO ever recorded, pricing at $135 a share for a valuation near $1.75 trillion. A rocket and satellite company is now one of the ten most valuable public companies on earth, and its first major move as a public entity was to buy an agent.

Look at what else sits inside the same company and the purchase stops looking like a developer tool. It starts looking like a final ingredient.

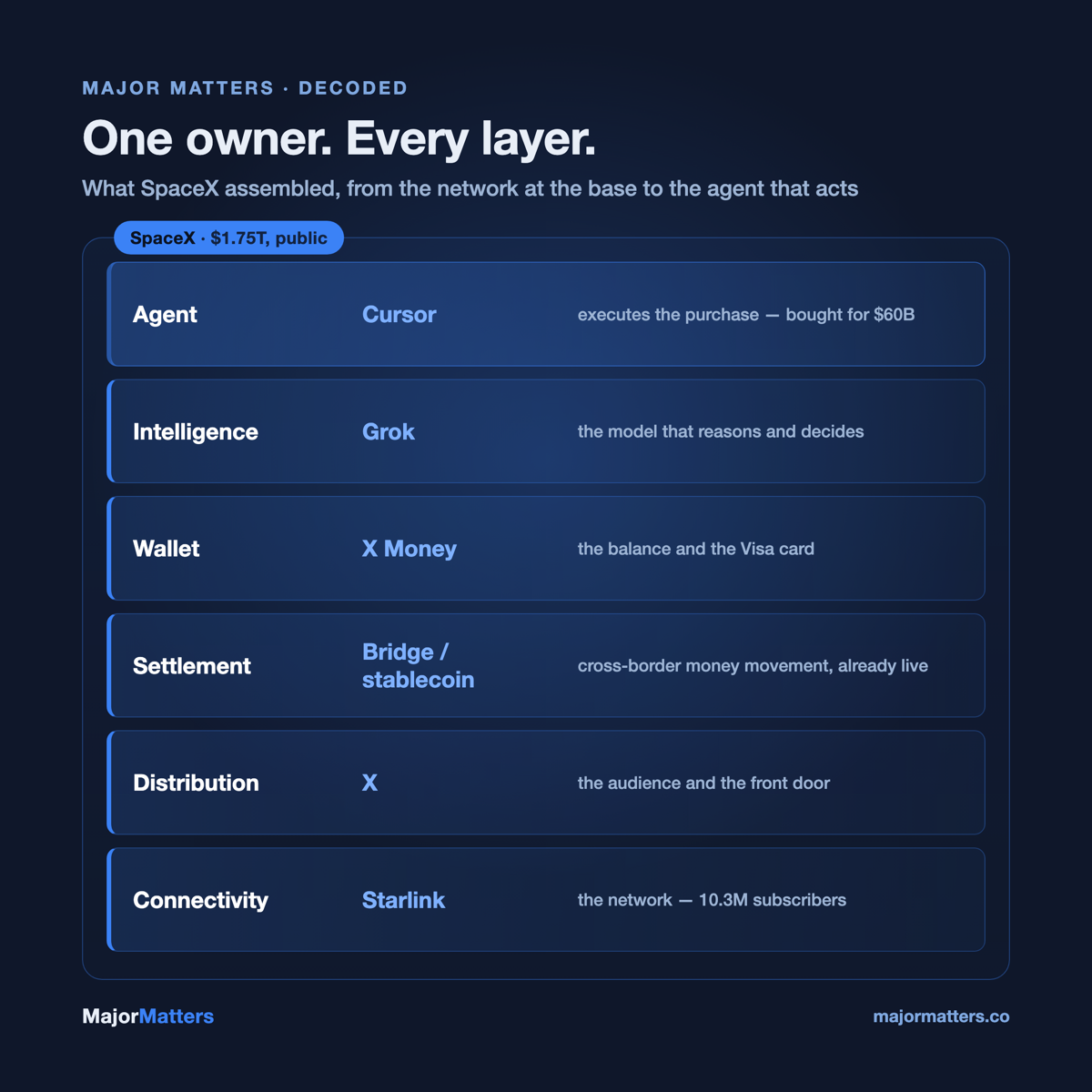

SpaceX now holds the network, the audience, the wallet, the model, and the agent. It is the first public company to own every layer commerce runs on, and almost nobody is describing it that way.

The stack nobody is counting

The parts were assembled quietly, in separate deals, each reported as its own story.

Starlink is the connectivity layer and the customer base. It ended March 2026 with 10.3 million subscribers and generated $11.4 billion in 2025, which was 61 percent of SpaceX's revenue and climbed to 69 percent in the first quarter of 2026. This is a consumer subscription business at global scale, billing households across more than 100 countries every month.

xAI is the intelligence layer. SpaceX absorbed xAI in February 2026 as a wholly owned subsidiary, then moved to fold its products, the Grok model and the social platform X, fully into the company. The result is that Grok, the X app, and its hundreds of millions of users now report up to the same parent as the satellites.

X Money is the wallet. It is the piece the coding coverage skipped entirely, and we will come back to it because it is the one that matters most to this publication's readers.

Cursor is the agent. It reached around $4 billion in annualized revenue by early June, more than doubling in four months, with more than 1 million paying users and 50,000 corporate clients, over half of them in the Fortune 500. It is the surface where a natural-language instruction becomes an executed action: write the code, run the command, open the file, make the change.

Five layers, one owner: connectivity, distribution, intelligence, a wallet, and now execution. A sixth, settlement, is already running underneath. Each arrived as a headline of its own. The system they form did not.

Why the agent was the missing piece

SpaceX described the Cursor deal as "a compelling extension of our strategy to vertically integrate compute infrastructure, models, and applications." The application layer is the part worth reading closely. An agent is where intent turns into action. A model answers a question. An agent does the task.

Cursor's value is not that it writes code. It is that it pursues a goal with little human supervision, opening files, running commands, and committing changes on its own. Move that capability from a codebase to a checkout and you have software that can browse, choose, and buy. Coding is simply where the pattern was proven and the revenue was found first. The underlying capability is general.

We have written about how value in agentic commerce migrates to whoever owns the agent that acts, in the week the payment rails moved inside the agent. Owning the execution surface is owning the point where commerce actually happens. Every other layer feeds it. SpaceX spent $60 billion to own that point.

X Money is the part the coding story missed

Here is the layer the acquisition coverage walked straight past.

X Money went to limited beta in March 2026 and opened to early public access in April. It ships a metal Visa debit card, deposits insured through Cross River Bank, peer-to-peer transfers over Visa Direct, and, as reported, a 6 percent yield and 3 percent cashback. Musk has been blunt about the ambition. He wants X Money to become "the place where all the money is, the central source of all monetary transactions."

Set that line beside the rest of the company. The agent that can act, the model that can reason, the feed where a vast audience already spends its attention, and a wallet already holding a balance and a card. An agent that meets you inside an app you open every day, funded by money you already keep there, is a far shorter path to an autonomous purchase than anything the standalone model labs can assemble. They have the agent. They do not have the wallet or the distribution.

The settlement layer is not a someday either. SpaceX disclosed on a 2024 earnings call that Starlink uses Bridge, the stablecoin infrastructure firm Stripe acquired for $1.1 billion, to repatriate revenue from markets like Argentina where dollar wires are slow and expensive. Part of the money already moves on programmable rails, in production, today.

The Visa question

There is a tension the launch coverage missed, and it is the one payments professionals should sit with.

X Money runs on Visa today. The debit card is a Visa card. The transfers use Visa Direct. The press read it as a Visa win, and for now that is exactly what it is.

Now look at the architecture rather than the launch partner. Once the wallet holds the balance, the agent starts the purchase, the model picks the merchant, and the network carries the distribution, the card rails become one option rather than a requirement. A transfer between two X Money wallets inside a closed system needs no interchange. Stablecoin settlement, which Starlink already runs, needs no card network at all. Musk's stated goal, the central source of all monetary transactions, is a description of disintermediation phrased as a product vision.

The question is not whether X Money rides Visa. It is how long it chooses to.

We have tracked the same gravitational pull across this beat. Adyen built a universal translator for agent payments that profits whenever the standards stay fragmented. Coinbase shipped spend limits that quietly productized the mandate primitive inside a regulated venue. The pattern holds. The companies that already own the customer and the money are the ones closest to running agent commerce, and several of them are building the parts that let them stop paying the middle. SpaceX has more of those parts than anyone.

A closed loop against an open standard

The rest of the industry is building the opposite of what SpaceX has.

The open agent-payment effort, from Google's portable mandate to the Agentic Commerce Protocol to Coinbase's x402, is a bet on interoperability. The goal is a shared standard so any agent can transact with any merchant through any wallet, carrying a verifiable mandate that proves the user approved the purchase. We argued that Google shipped the only agent payment mandate that travels, and portability is the whole point of that camp.

SpaceX is building a closed loop. One owner of the agent, the model, the wallet, the network, and the audience does not need an interoperable standard inside its own walls. It needs no one's permission and pays no one's toll. That is either the most efficient path to working agent commerce or the largest concentration of commercial control under a single founder the payments world has seen. It is both at once.

The two camps even fail differently. The open standard has to solve trust between strangers: how a merchant confirms that an unfamiliar agent is genuinely authorized to spend. The closed loop solves that by owning both ends of every transaction, and inherits a different exposure instead, where pricing, access, and fairness all rest on one company's judgment.

The data the stack produces

Vertical integration buys SpaceX more than control. It produces a feedback loop that no single-layer rival can match.

Each layer generates a different kind of behavioral data, and all of it now pools under one owner. Cursor captures how work gets done, the verifiable coding behavior that SpaceX itself noted can sharpen model training. X captures what hundreds of millions of people pay attention to. X Money captures how they spend and save. Starlink captures where and how they connect, across more than 100 countries. Coding behavior, attention, money, and connectivity, feeding the same models that drive the same agents that move funds through the same wallet.

A commerce agent is only as good as its read on the customer. SpaceX is assembling the widest read available to any company, because it owns the surfaces where the behavior happens rather than buying the exhaust secondhand. That is the quiet compounding advantage underneath the headline price. The $60 billion bought an agent. The data that agent generates is what makes the next one better.

What is not there yet

None of this has shipped as a commerce product, and the honest version of this story says so plainly.

Cursor writes software, not shopping carts. There is no Grok agent buying groceries through X Money, and SpaceX has announced no plan to build one. The stack is assembled. The commerce application on top of it is a thesis, not a release.

The settlement layer is rented, not owned. Starlink uses Bridge, which Stripe owns. X Money runs on Visa. SpaceX holds the demand and the distribution today, not the rails beneath them. Owning the customer is not the same as owning the clearing.

The structure also invites scrutiny. The $4 billion antitrust break fee is an admission that concentration is a genuine risk to closing the deal. X Money has already drawn attention from Washington, with the Senate Banking Committee writing to Musk in April with questions about the launch. A company this large folding payments, AI, a social network, and global connectivity under one roof is exactly the kind of structure regulators examine slowly and carefully.

And the integration carries its own friction. Once the deal closes, SpaceX has every incentive to make Grok the cheap default inside Cursor, which raises a fair question about whether the best model wins there or simply the in-house one.

What to watch

The thesis is testable, and the signals are specific.

Watch for a Grok agent that can transact rather than only answer. Watch for X Money to add wallet-to-wallet or stablecoin settlement that routes around the card networks. Watch for Cursor's agent framework to surface outside developer tooling, in booking, shopping, or bill payment. Watch whether Starlink's stablecoin repatriation moves from back-office treasury plumbing to a consumer-facing rail.

Any one of those turns an assembled stack into a working agent-commerce business. Until then, SpaceX has done something quieter than a coding headline suggests. It has gathered every piece the rest of the industry is still trying to standardize, and it owns all of them.

The infrastructure is ahead of the demand. The difference, this time, is that one company owns the whole of it.

Sources

- CNBC: SpaceX to acquire Cursor for $60 billion

- TechCrunch: SpaceX prices shares at $135 in the largest IPO ever

- CNBC: Starlink growth, profit and the Nasdaq IPO

- The D&O Diary: The SpaceX and xAI merger

- PYMNTS: Musk says X Money to debut in April

- CBS News: What is X Money, Elon Musk's payments platform

- a16z: What Stripe's acquisition of Bridge means for stablecoins

- US Senate Banking Committee: Letter to Musk on X Money

If the company that owns the agent also owns the wallet, the network, and the model, what is left for the rest of the payments stack to charge for?

Charlie Major is a Product Development Manager at Mastercard. The views and opinions expressed in Major Matters are his own and do not represent those of Mastercard.